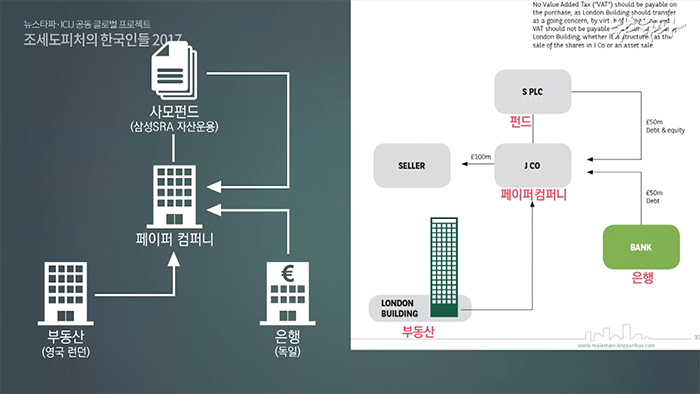

In 2013, Samsung SRA Asset Management, an affiliate of Samsung Life Insurance, purchased a 16-story building located in central London by establishing a private equity fund (PEF) called 'Samsung SRA Private Real Estate Investment Trust #2.'

Korea’s large-scale institutional investors like Samsung Life Insurance, Samsung Fire & Marine, Kyobo Life and Shinhan Life Insurance joined this investment.

KCIJ-Newstapa identified multiple pieces of internal documents related to this deal from a pile of data leaked from the Bermuda-based law firm Appleby. The documents clearly showed the global investment funds’ tax dodging tactics carried out as part of what they call ‘industry practice.’

Samsung SRA Asset Management bought in a London property via a Cayman-based shell company

The building at 30 Crown Place, London is a golden piece of property, as London’s famous law firm Pinsent Mason is using office spaces generating stable amount of lease income.'Samsung SRA Private Real Estate Investment Trust #2' paid about 145 million pounds to purchase the building, about 250 billion won by the exchange rate back then.

After purchasing this building, the Samsung SRA fund has reportedly recorded a return of nearly 20 percent. However, the fund has never held a legal ownership over the building.

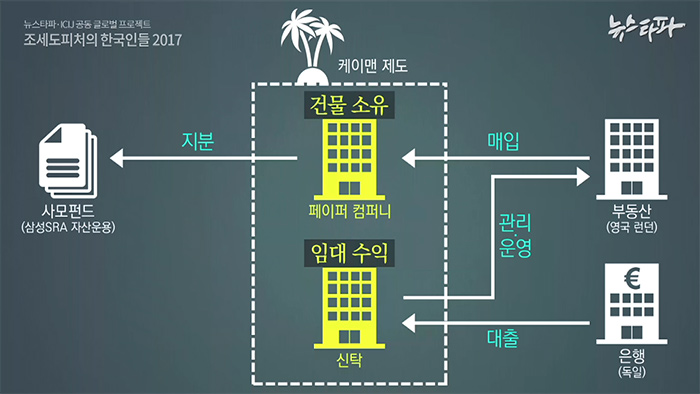

What’s behind the ownership structure?

According to Paradise Papers documents leaked from Appleby, the building’s ownership structure is explained in detail.

Firstly, Samsung SRA incorporated a trust in the Cayman Islands and made a shell company to own this trust. Then, it made the trust purchase the London building, while making the Samsung SRA PEF to own shares of this shell company.

In separate, it established a trust company and made it manage and operate the London building.

About half of the building’s acquisition cost was secured by borrowing from a German bank, but Samsung SRA made the loan issued to the trust company, not the PEF.

Under such a structure, a Cayman-based shell company got to become a legal owner of the building, not a Korean fund. Thus, this building's lease income has belonged to the Cayman-based trust company.

Designed the complex structure for tax reduction … a common industry practice?

Why does a PEF need such a complex ownership structure when investing in a British property?

Clues to the answer were found in an investment promotion booklet from BNP Paribas last year. The booklet encourages readers to invest in London properties, providing various investment tips. Many of the tips were aimed for tax reduction.

Various tax-cutting tactics were introduced based on a Singaporean investor's case with a London property, and the structure is very similar to that Samsung SRA used.

The Singaporean investor purchased the real estate through a shell company based in the Bailiwick of Jersey, and made the shell company borrow half of the acquisition cost from a bank.

The BNP Paribas booklet named following points as advantages of this complex structure:

Firstly, the structure allows investors to avoid a transfer tax (stamp duty land tax), worth nearly 4 percent in the property's price. In this structure, no tax occurs as there is no direct transaction as all transactions are made indirectly by buying a shell company’s shares.

Secondly, the building's lease income belongs to the shell company. So, the shell company only gets to pay tax for the remaining amount -- after paying interests for the loan and paying dividends for mother companies like the Singaporean investment company or Samsung SRA PEF. In addition, the amount of tax is substantially low as the shell company has been incorporated in Jersey, a tax haven. This greatly helps reducing tax expenditure.

Under this structure, property deals actually happens in the U.K. and the Singaporean investor or Samsung SRA makes money by leasing the office spaces.

However, in conclusion, the amount of tax paid to the British tax authority is nearly zero pound.

When KCIJ-Newstapa made an inquiry about this, Samsung SRA Asset Management acknowledged that it made the transaction via a shell company to avoid tax.However, it at the same time explained that such a method is a common practice in the investment industry, and that it doesn't consider this method problematic as it avoided tax in the U.K, not in Korea, to give back higher returns to investors at home.

How is it different from Lone Star’s case?

On Oct. 24, Lone Star Funds won at the final round of trials on a lawsuit it filed against Korean National Tax Service (NTS).The trials initially started as the NTS imposed a corporate tax of 170 billion won ($151.64 million) for its profit margin it gained while selling the Korea Exchange Bank shares in 2007. The funds filed a lawsuit saying that the corporate tax was unfair. It was one of many lawsuits filed from Lone Star against the Korean government.

After years, the trials came to an end with Lone Star's victory, because it invested via a shell company based in various tax havens like Belgium and Bermuda -- instead of directly making investment in Korea.

"Major investors in the Lone Star Funds were foreign corporate entities with no fixed places of business in Korea, thus it is unfair to impose corporate tax on them," the Supreme Court of Korea ruling read referring to the ruling made in the first trial.

As a result, Lone Star avoided taxation from the Korean tax authority after earning a massive profit margin by buying an asset and selling it off here in Korea.

Many Korean media outlets criticized such a tactic to be ‘eat and run,’ an action of taking advantage when the Korean bank was ailing and selling it soon evading tax.

Then, how are the two cases different from each other: Samsung SRA’s case, which avoided British taxation while enjoying a massive profit margin in the process of trading a London-based property through a Cayman-based shell company, and Lone Star’s case in Korea.

Jun Sung-in, Professor at Hongik University School of Economics, analyzed the two cases.

“Having no fixed places of business in Korea and England, both companies tried to avoid taxation from these countries while making profits there,” Jun said. “Both cases utilized Double Tax Avoidance Agreement as a means of reducing amount of tax, by claiming that they would pay tax to a jurisdiction where it established the fund.”

This way, the two companies could have been able to save additional amount in tax by establishing the fund in a tax haven where tax rate is substantially lower than the countries where profits generated, Jun added.

Tax avoidance a ‘common practice’ for the super rich of top 1%

Samsung SRA, a Korean capital, tried to avoid tax in the U.K. while American capital Lone Star tried to avoid tax in Korea. Do these situations make a tie?

This issue may feel entirely different if looking at this as a taxation issue between income groups -- not a race among capitals of different nationalities.

Whether such a problem occurs in the U.S. or in Korea, tax reduction benefits through a tax haven cannot be enjoyed by everyone.

Top 1 percent of population by income is the largest beneficiary of this system.

Of course, the rest of 99 percent commoners could join this type of investments by installing small amount of money in a fund or an insurance product. However, the size of financial returns or benefits would be incomparably different.

If the super wealthy keeps expanding its wealth with their tax reduction technique, there is no other way but the 99 percent of moderate income earners get to fill in the gap in the government’s tax revenue.

In this regard, the investment industry’s long-standing practice cannot be rationalized.

Tax Justice Network, an international civic group, estimates that about $21 trillion to $31 trillion of assets globally are held offshore.

As the current system virtually allows the top 1 percent of population avoid tax hurting each country's tax revenue, the system at the same time puts the tax burden on the 99 percent moderate income earners to fill in the gap in each government's treasury.